Read this article in Français Deutsch Italiano Português Español

ING highlights a challenging year ahead for Euro construction

20 March 2024

Market analyst ING Research has forecast a challenging year ahead for European construction businesses, despite the fact that there was marginal growth in construction output in 2023.

Across the EU, output grew by an average 0.1% in 2023, largely due to a relatively strong performance in the first quarter.

The third and fourth quarters of the year, however, saw output decline by 0.3% and 0.2% respectively, following interest rate growth and a subsequent reduction in investor interest.

ING did point out that the number of renovation projects progressing held firm, due primarily to initiatives put forward by the European Commission and continuing investments in digital infrastructure.

The analyst reported that a reduction of 0.5% in output volume is expected in 2024, driven down by a reduction in new residential and non-residential construction.

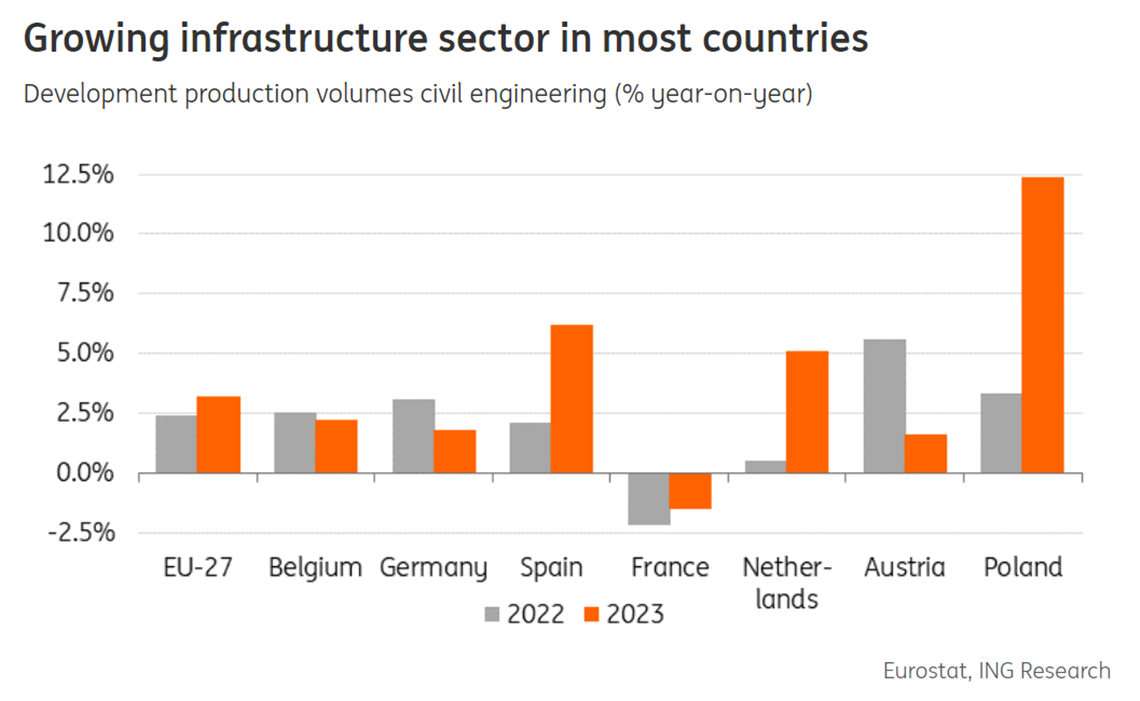

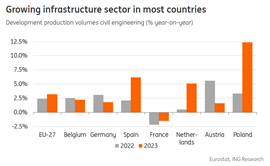

Infrastructure in relatively good shape

Investment in infrastructure projects, however, should continue to rise, partly driven by continued funding from the EU Recovery and Resilience Facility, as well as the growth in new energy projects.

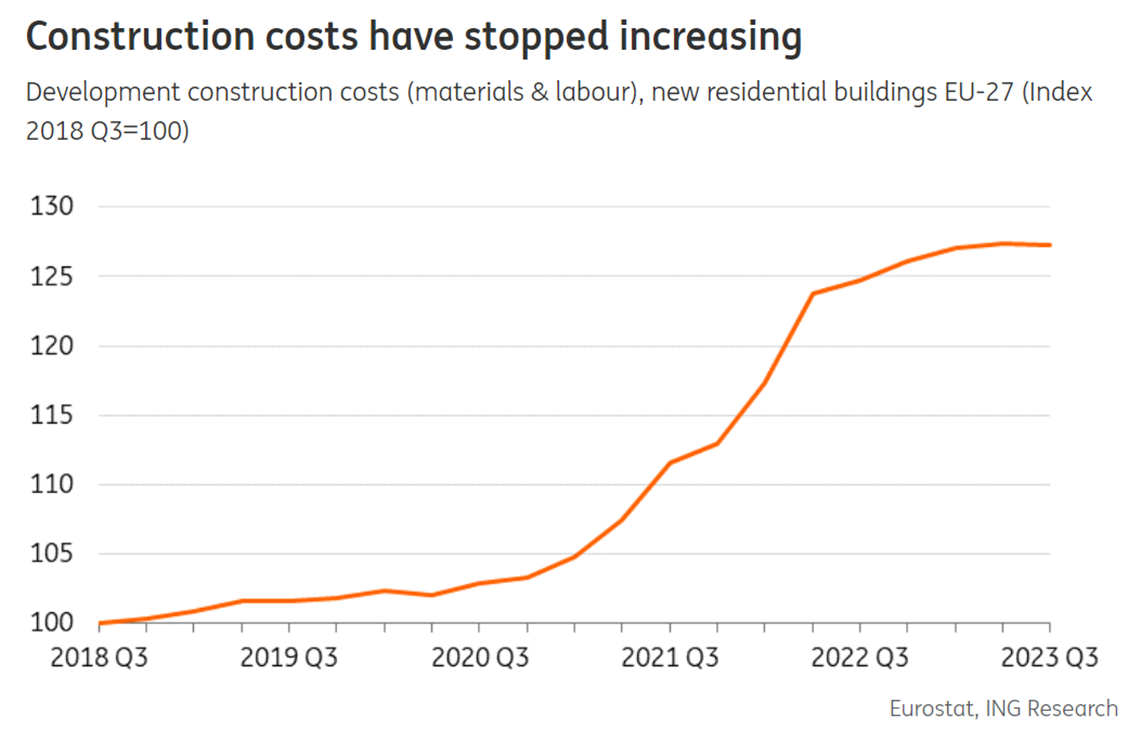

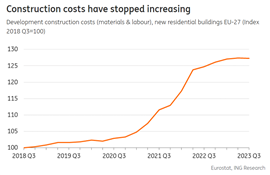

It would also appear that the rise in materials prices and general construction costs have peaked, although it may be some time before a reduction in the cost of materials such as cement will be seen.

The ING report describes positive trends continuing in the renovation and infrastructure sectors into 2025.

For EU-based contractors, for example, order books appear to be extremely stable, with 9.1 months of work currently the average in the portfolios of businesses, which is similar to the 2023 figure.

ING suggests the growth in the number of renovation and sustainability projects is a primary reason for this relatively strong showing.

Another possibility is that the increasing complexity of large infrastructure projects is increasing the scope of work and therefore the time required for construction to be completed.

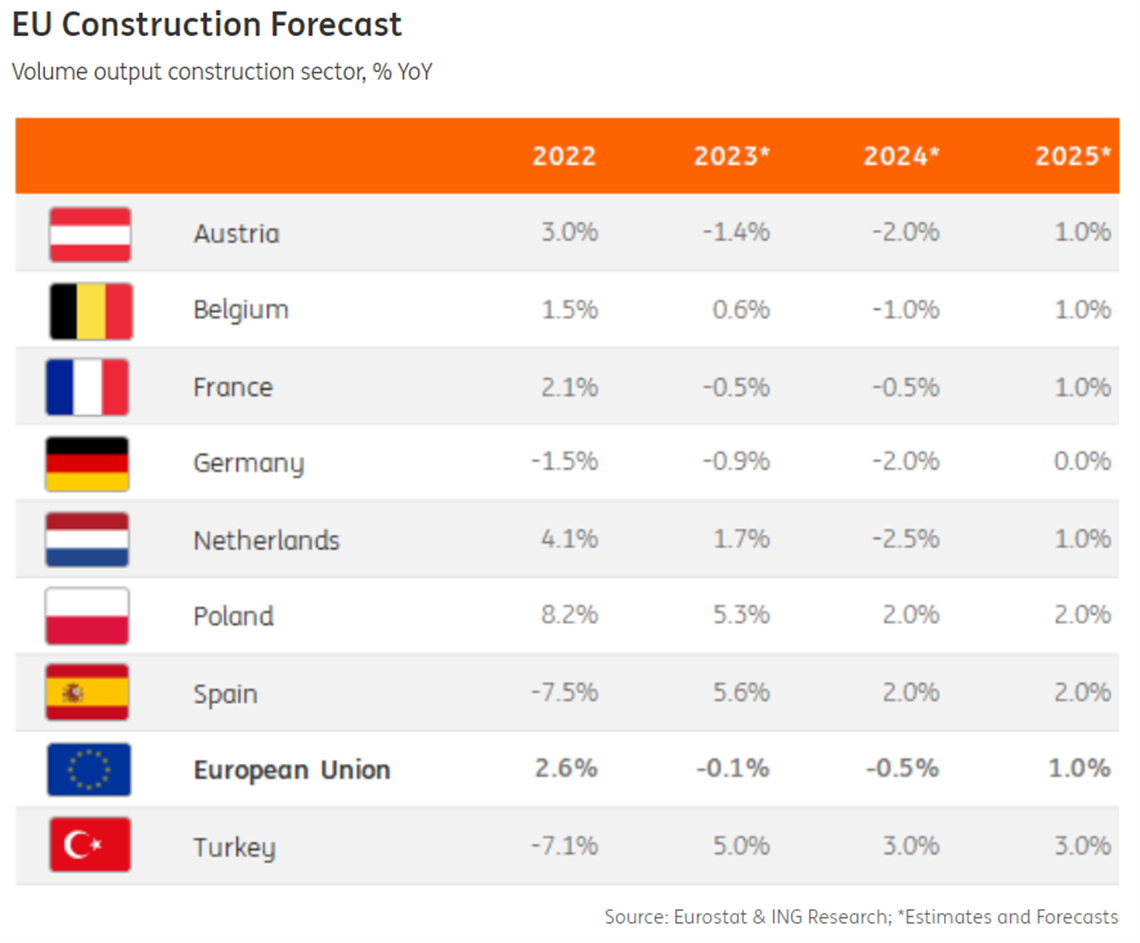

Key countries snapshotHere, ING gives its forecast for the year in construction for 7 major markets in Europe Belgium The Belgian construction confidence index entered negative territory in 2023. Yet, Belgian construction output still showed an increase last year due to the late cyclical nature of the sector due to long lead times from building projects. Looking ahead to 2024, we expect more challenges and we expect a slight decline. The issuance of building permits for residential buildings has decreased in the last two years, but more moderately than in other countries. There are still structural drivers: the infrastructure needs an upgrade, 85% of the homes do not currently meet the 2050 energy standards and housing shortages persist. We therefore expect that growth will return in 2025. France French contractor sentiment has become gradually pessimistic in 2023. In February, the French construction confidence index (EC survey) was still marginally negative. In addition, French construction order books are a bit less well-filled. French contractors now (1Q 2024) have 7.9 months of work on average in their backlogs compared to 8.1 months in the first quarter of last year. Yet, compared to the long-term trend this is still relatively high. The issuing of building permits for new houses is also decreasing, but at a slower pace than in many other countries. Labour shortages are less of an issue but are still relatively high. Government measures such as MaPrimRénov are supporting renovation and sustainability activity. For 2024, the budget of this scheme has increased from €2.5 to €4 billion. The plan was first to increase the budget to €5bn but due to budget restraints it has been decreased. Overall, we expect that French construction output will decrease marginally by 0.5% in 2024. Germany In 2023, German construction activity decreased by 0.9% after already experiencing two years of decline in 2021 and 2022. For 2024, we forecast a further moderate contraction of the largest construction market in the EU. While the order book assessment of contractors in the EU remains stable, German building companies have faced a decline to 3.6 months of work in the first quarter of 2024, down from 4.5 months a year earlier. A further decline in building permits for new residential buildings during the third quarter of 2023 signals ongoing challenges. The bankruptcy of several project developers last year due to high building costs exacerbates the situation. Consequently, the government target of 400,000 newly built houses won’t be reached this or next. Yet, the German civil engineering sector provides some counterbalance. German infrastructure is in a dire state and investments in roads and digital infrastructure foster some growth in this subsector. Netherlands As in other countries, the issuing of building permits in the Netherlands has decreased enormously in the previous quarters. Yet, demand for new houses is picking up and the number of new houses sold has increased in the last few months. For instance, in February, this increased by more than 50% compared to the same month in 2023. However, as in other countries, the pain of previous sales declines still has to be taken in 2024 and the permit issuing has to increase as well before we see growth again in 2025. Many major Dutch infrastructure projects are experiencing delays due to the nitrogen issue and higher-than-expected costs. The government has therefore decided that many new infrastructure projects will be temporarily put on hold (not meaning cancellation). Projects that have already begun will be completed. However, the budget for the maintenance of railroads will increase in the coming years. Poland In Poland, the construction sector grew by 5.3% last year. The higher volumes were mainly driven by the infrastructure sector. The beginning of 2024 was less promising, Polish construction output fell 6.1% in January (year-on-year) as many projects under the previous EU financial perspective have ended. The startup of new EU-financed projects will take some time. Also, the building sector is performing less well. Building permits for residential buildings decreased by 6% in the third quarter of 2023 (YoY). That said, in February, the construction confidence indicator was still higher than in the same period a year earlier and contractors were also more satisfied with their order books, which are well filled with 8.8 months of work. Overall, we anticipate that total Polish construction output will still grow this and next year but at a slower pace than in the previous two years. Spain The Spanish construction sector grew by a very solid 5.6% in 2023. This looks impressive but we shouldn’t forget that the industry has seen some bad years. By the end of 2022, the production level was almost 25% lower than it was at the end of 2019. Yet order books are now improving and have touched the highest point in the first quarter of this year since 2006. The EU’s recovery fund investments in the Spanish construction sector generate a more positive outcome moving forward. The increase in building permits will also have a positive effect on building volumes. Yet the question will remain as to how many approved projects will actually be built as challenging circumstances persist. Nevertheless, we expect further growth in the Spanish construction sector in 2024 and 2025. Turkey For the first time in five years, the Turkish construction sector grew in 2023. Production volumes increased by 5%. In February, the Turkish construction confidence indicator (EC survey) showed a negative reading of -7.4. Still negative, but it has been slightly improving in the last six months. However, order books recovered slightly in 2023 but fell back in the first quarter of 2024. Fewer Turkish contractors are complaining about low demand, and the issuing of building permits is pretty much stable. The earthquakes in 2023 have caused massive damage to over 300,000 buildings. The aim is to rebuild approximately half of this within one year. This drives up demand for building materials and construction workers. Our expectation is that reconstruction efforts will generate further growth in the Turkish construction sector in 2024. |

STAY CONNECTED

Receive the information you need when you need it through our world-leading magazines, newsletters and daily briefings.

CONNECT WITH THE TEAM